Sequim Real Estate: Our 6 Most Popular Articles of 2016

This Sequim Real Estate Blog is by far the largest local real estate blog in Sequim and possibly the largest...

This Sequim Real Estate Blog is by far the largest local real estate blog in Sequim and possibly the largest...

What will happen to the Sequim real estate market this coming year? What will prices do? What will the Sequim...

I have a client who found a home he really liked, and it immediately went under contract. In fact, it...

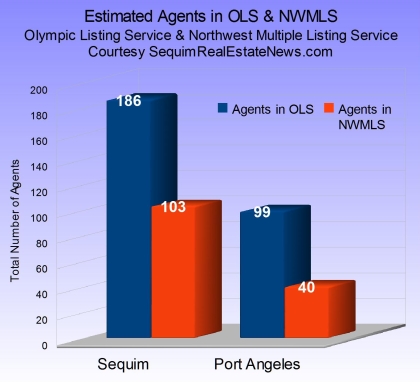

Sequim real estate listings and the shortage of homes that retirees want has created a difficult market and a slow down...

This is the place to get your real estate questions answered, but we have a very unique approach. Earnest Hemingway...

Attic ventilation is one of the important items on a long checklist of things to watch for when you buy...

We are excited to announce the all new 4th edition of Sequim Real Estate: A Buyer's Guide, which is now...

Some home sales are terminated before closing. A client from California asked me today, "What are the main reasons that...

Do you know how to search the Internet for real estate? Today I want to share how to search the...

This Sequim real estate blog can be read on mobile devices on your iPad or your Kindle or on any tablet....

Do you have real estate questions? Questions about Sequim, Port Angeles, or Port Townsend? Questions about retiring on the Olympic...

Veteran's Day is an important day, and I'm grateful for our veterans who protect this great nation and our freedom. Some...

What's a Sequim interview deluxe? It is the Buyer's ultimate interview about Sequim. Let's set the context so I explain...

Chuck Marunde created a number of Sequim real estate checklists over the past two decades, and buyers from around the...

Let's compare the San Juan Islands with Sequim. If you're planning to retire to the great Northwest from California or...

This new Sequim property is right at the top of the Bell Curve for retirees moving to Sequim. One person said to...

Sequim listings can be dramatically different. Do not assume that all sellers and their listing agents are on the same...

Sequim homes are hot right now. Many buyers are experiencing some frustration, because when they find what they think could...

Researching real estate on the Internet is now done by almost 100% of all buyers. Researching real estate for most people...

This may be the most powerful Sequim real estate search tool on the Net, and as a buyer it is...

"I wish I read this before selling my

home. I could have saved $50,000." Andy

The largest independent real estate blog in the State of Washington with over 2,200 articles totally focused on our client’s best interest, their needs and their curiosity. All free and 100% reliable. I’m here if you need me,