A bump clause is a special clause in an addendum to a purchase and sale agreement that gives a seller the right to continue to accept other offers and possibly bump the first offer out of the picture entirely. This means a bump clause can either help a seller or hurt a buyer. In this article I’ll explain when and how to use a bump clause.

Bump Clause Favoring the Seller

When does a bump clause come up? When you make an offer on a property, you may offer all cash or maybe you’re going to apply for a loan. There is no bump clause involved in those cases, but if you are going to make an offer contingent on the sale of your existing home, there is a bump clause in that addendum.

Not all sellers will accept an offer contingent on the sale of the buyer’s home, but if they do, the form in Washington is a “Form 22B Buyer’s Sale of Property Contingency.” The bump clause gives the buyer a specific number of days to get the sale of their current home under contract, and if they don’t have it under contract, the entire transaction is terminated. While it is pending, the bump clause gives the seller the right to accept better offers and give you, the buyer, a notice that you can either waive your contingency or the transaction is terminated and the seller will sell the home to the other buyer.

Some buyers will cross this bump clause out so the seller cannot bump their offer, but a seller may reject that, too.

Bump Clause Favoring the Buyer

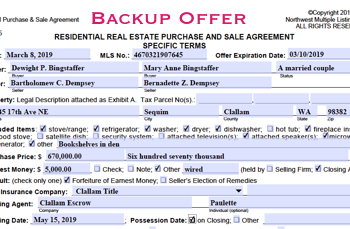

If you get a seller to agree to accept an offer that is contingent on the sale of your current home with a bump clause crossed out, like in the image above, then that clearly favors you as a buyer. Who wants to get bumped, right? On the other hand, a seller doesn’t want to take his home off the market for several months waiting for you to sell your current home either.

All of this boils down to whether it is a seller’s market or a buyer’s market, and how motivated the seller is to accept an offer with a bump clause.

Last Updated on August 26, 2017 by Chuck Marunde