What happens when a buyer’s financing falls through and they want to terminate the contract and get their earnest money back? Can they?

Let’s be clear that if a buyer’s financing fails to get approved within the deadline of a pending contract, the buyer has the right to issue a proper notice to the listing agent (the seller) of that failure and their desire to terminate the contract and have their earnest money returned. The typical case is where the buyer can’t qualify for the loan, or interest rates went up suddenly, and the buyer is no longer qualified, or a credit agency picked up a new black mark on the buyer’s credit, and they no longer can meet the underwriting standards.

In such a typical scenario, the buyer issues a proper notice prior to the deadline, and the parties both sign a release of the earnest money so the escrow company can refund the earnest money to the buyer. That is the end of the story for most transactions that fail because the buyer cannot qualify for a loan.

But what if the buyer does not yet have their financing approved by the time of the closing date. Even though they have not waived their financing contingency, can they submit a notice to terminate after the closing date to the listing agent (the seller), and would they be entitled to the return of their earnest money?

Even before the closing date, under what conditions can the buyer back out and still get their earnest money back? I’ll answer these questions, but the focus of this article will address a unique scenario that just happened in the Seattle area. I received a call from a listing broker with an interesting fact pattern. Here’s a brief picture of what happened.

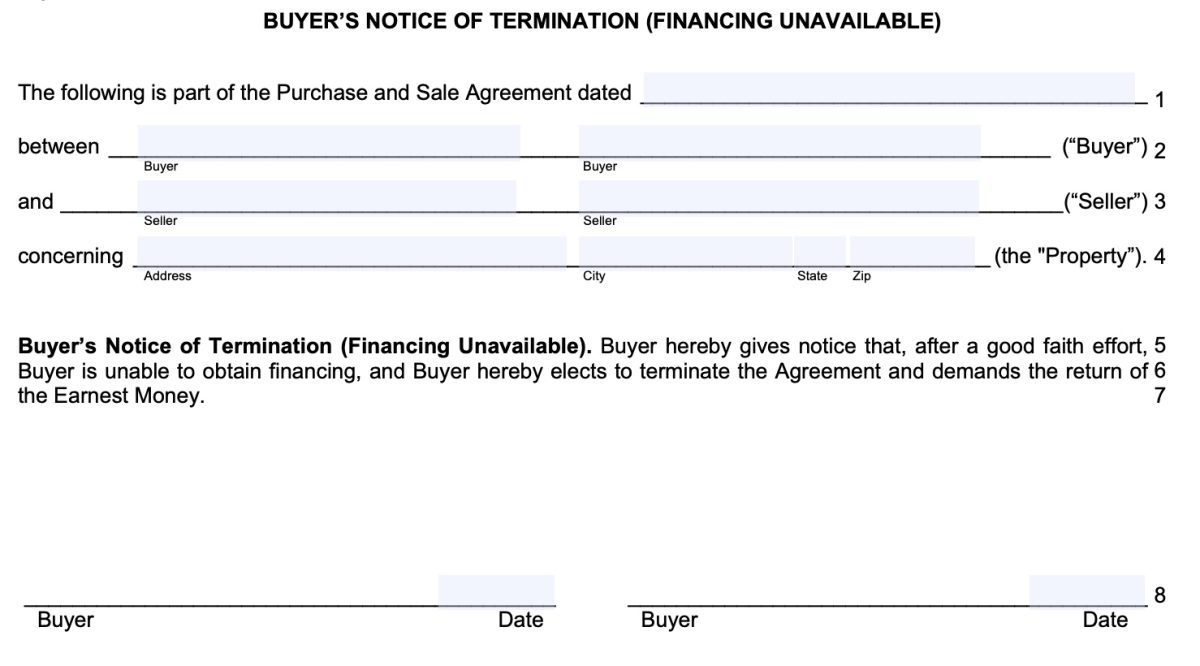

- The buyer’s financing was not approved, but the buyer did not give notice to the listing agent (the seller) until one day after the closing date. The notice the buyer’s agent gave the listing agent one day after the closing date was a Form 90I (See image below) and a Form 50 (Rescission–The wrong form to use when terminating on a financing issue. See my full article on the mistake of using rescission instead of termination, another big mistake made by most of Washington’s brokers and wrongly promoted by the Legal Hotline Attorneys).

- The Form 90I notice only stated that the buyer was unable to obtain financing, but no contractually justified reason was given, and no bank documentation was attached at the time for the bank’s reason.

- The buyer’s agent did not provide any proof or documentation from the buyer’s lender as to why their loan was not approved until almost three weeks past the closing date.

- When the listing broker received a copy of the email addressed to the buyer with the explanation from the buyer’s bank, it simply stated that the buyer’s financing was not approved because their debt to income ratio (DTI) was outside the guidelines. The buyer’s own bank did not even give them notification by email until the day after closing.

- The buyer’s agent insists that the seller release the earnest money to them.

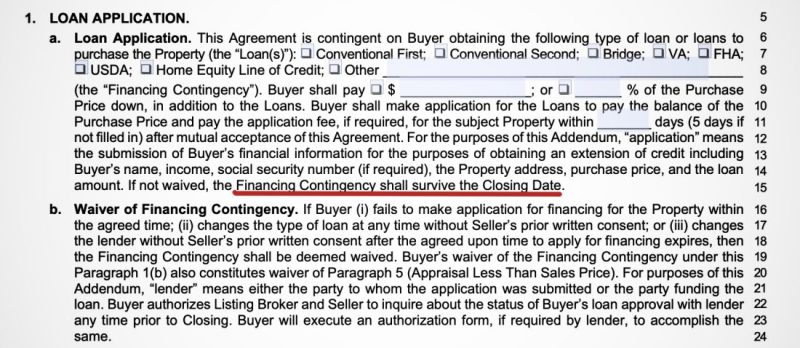

The buyer’s agent argued that the buyer was entitled to his earnest money back based exclusively on a clause in the above Washington Form 22A Financing Addendum, which states:

“If not waived, the Financing Addendum shall survive the closing date.”

In order for the Financing Addendum to survive the closing date, there must be a contractual authorization to close beyond the official closing date. We’ll discover the narrow conditions that would authorize an extension later in this article.

The buyer’s broker wrote:

“The buyer is entitled to a refund of the earnest money since the buyer did not waive the financing contingency. The buyers did act in good faith to obtain the loan.”

What the buyer’s broker is arguing is the same as this paraphrase:

“The reason the buyer is entitled to a refund of the earnest money is because the buyer–by his silence–did not waive the financing contingency, and since the buyer did not waive the financing contingency, the closing date, which would normally be the natural end of a contract, is extended in perpetuity, and the buyer has no time limit on issuing a termination after the closing date, which justifies a return of the earnest money to the buyer.”

Of course, that broker is likely to say, “I didn’t say the closing date is extended in perpetuity!” Then the question to that broker is, “Well, then how do you define a deadline for your buyer? What are the contract terms that identify when and how your buyer can terminate post closing date and get their EM back?” Of course, the broker won’t be able to answer that question, because she is shooting from the hip and cannot justify her unsupported legal opinion.

The buyer’s broker’s statement is made without any justification or support from the contract language or case law. The statement is incorrect, and I’ll explain why.

Everyone is a lawyer!

The buyer’s agent’s argument is that the clause that states the “Financing Addendum shall survive the closing date” means that the buyers can revive the PSA (Purchase and Sale Agreement) after the closing date for purposes of trying to terminate the transaction and get their earnest money back.

This clause has been the source of endless discussions among brokers, and has been the source of mass confusion and different opinions about what rights and responsibilities it creates for buyers and sellers when a buyer’s financing fails. Even their attorneys have been confused about the meaning of this clause in the Form 22A Financing Addendum. To state the obvious, the clause is poorly drafted. It is legally ambiguous. But the fact that it is poorly drafted and legally ambiguous does give a broker the right to assign any meaning to it that suits their client’s needs.

There are several fundamental contract law principles that are violated with the buyer’s agent’s interpretation.

Contract Expiration at Closing: It is basic contract law that a contract expires or dies a natural death on the closing date. The closing date represents the last day of the contract. That closing date can be extended by an extension signed by both parties, but when the final closing date is reached, the contract provisions all expire with the contract.

Exceptions That Extend The Closing Date Without a Signed Extension: Case law in Washington has extended the closing date when there is an event beyond the buyer’s control and not caused by them that requires a short extension of the closing, usually a matter of days. Such court ordered extensions typically involve an unanticipated delay in an appraisal or in underwriting approval or some additional inspection that had to be done before final underwriting approval. It’s always a case in which the buyer wants to proceed to closing, and is ready, willing, and able, but a third party, like a mortgage company, cannot procedurally fund or close until a short time after the designated closing date.

Contract Extension or Revival: There’s a difference between a contract extension and a contract revival. In order for a contract to be extended beyond its final date, there must be a signed agreement by the parties or there must be a contract provision within the contract that automatically is triggered to extend the closing date. When a contract expires without any authorized extension, it dies a natural death on that final date, and once a contract has officially died, you cannot extend it, nor can any contract clause extend it, because first you would have to revive the contract. Only an active contract can be extended. Only a dead contract can be revived.

Clearly the buyer’s agent and her legal cohorts, who are all shooting from the hip with a sentence or two in emails rather than do a thorough factual and legal analysis akin to what I am doing in this article, are arguing that the contract did not expire on the closing date, but was extended by the buyers by giving notice one day after the closing date that the buyer’s bank notified them that they did not satisfy the DTI guidelines.

The fact is they did not give notice (Form 90I) until one day after the contract died a natural death on the closing date. The only authorized contractual basis upon which they could have extended the contract is to give a proper notice of the financing failure prior to the contract expiration date (the closing date). They did not do that, and their subsequent notice did not have the legal power to revive a dead contract.

What About The “Survive the Closing Date” Argument?

First, the purpose of the Form 90I notice to terminate based on the financing failure must be issued prior to the contract expiration date (and it was not here), but even if it is issued prior to the expiration date, what does it mean to “survive the closing date?”

Contract law and judicial interpretation of contract law principles teach us that a contract is to be interpreted by what it says literally and by what it does not say. If there is an ambiguity, you can’t just make things up. In such a case, the context of the clause, any related clauses, and common sense will be applied.

If defies common sense and logic to argue that a buyer can claim the “survive the closing date” means they can extend the closing date for as long as they want. Of course, no buyer or their broker would argue they could extend forever, but isn’t that what they are claiming when they say it applies here?

The buyer’s broker argues that since the buyers did not waive their financing contingency (and that is accomplished by silence), they can extend the closing date unilaterally because of the sentence stating that, “If not waived, the Financing Addendum shall survive the closing date.”

What survives the closing date? And how long does such a contract right last beyond the closing date? A few days? A few weeks? Months? Years? No judge would agree that this ambiguous clause gives the buyer the right to keep a contract alive past its closing date when the buyer didn’t give any notice to terminate before the closing date.

The survival clause certainly does not automatically extend a contractual deadline for notice of termination beyond the closing date. I don’t know of any judge anywhere in Washington state, and I’ve argued in a dozen counties, who would agree that a buyer could extend any notice deadline beyond the closing date. Notices of all kinds within a contract like this must be given by the notice deadline, but within that deadline a notice could extend the closing date in a very narrow exception in this contract, and the conditions for that kind of exception are given in this Financing Addendum at the end under Para 9.

This last paragraph is tied directly to the survival clause in the first paragraph of this Financing Addendum. The context, of course, is the issue of financing. The two places in this Financing Addendum that use the word “survive” in the context of forcing an extension of the closing date are para 1a and para 9.

We can get some help in interpreting the related clause in 1a by examining the clause in 9. Para 9 lays out three conditions that entitle the buyer to extend the closing beyond the official closing date. Those conditions involve a required Reg Z disclosure that by Federal law extends beyond the closing date by a matter of one to three days. If these three conditions are met, Federal law trumps the closing date, but in this case the contract recognizes Federal law as a contractual basis to extend the closing date. The three conditions are:

- a change in the APR by .125% or more for a fixed rate loan, or

- a change in the loan product (i.e. a HUD loan program expires and a different loan can be used), or

- the addition of a prepayment penalty.

It is in the same para in the last sentence where it states, “This paragraph shall survive Buyer’s waiver of this Financing Contingency.”

If the buyer did waive their financing contingency or if it was waived by virtue of contract terms, which can include exceeding contractual deadlines that end the buyer’s financing contingency, then Para 9 authorizes the survival of that waiver to allow an extension of the closing date provided one or more of the three conditions in Para 9 applied.

But this para allows an extension of the closing date under very narrow conditions, and it does not give the buyer the right to terminate after the closing date and get their earnest money back. Such an argument is way beyond the scope of this contract and the Financing Addendum.

What Really Happened?

What I learned after many years of law practice is that there are usually some facts that no one is talking about that are really the driving force, and making specious legal arguments is often a cover for big mistakes that were made and which no one wants to talk about, mostly because of liability.

In other words, life teaches us that people are motivated by hidden agendas, and then there’s another phrase I think explains a lot of irrational or selfish behavior: “Follow the money.”

I’m not saying such hidden agendas apply in this case, but here are some likely motivations that I saw over and over again as a practicing attorney.

- Brokers are humans, and humans make mistakes. If the buyer’s broker missed the deadline to issue a notice to the listing broker before the closing date, she is most definitely not going to tell a soul, because that would instantly mean she could be liable to pay the buyers back all their earnest money. Granted, the bank in this case apparently did not send an email to the buyers until a day after closing, but were there not multiple communications prior to closing about potential problems with the buyer’s loan? There must have been. There always are. It is likely that the buyer’s broker didn’t have the knowledge and experience on the legal issues to handle this proactively to assure her clients could terminate and get their earnest money back.

- The buyer’s broker works for a broker/owner or franchise, and there is a designated broker who is responsible for supervising and reviewing all the brokers’ files. It appears that brokerage failed in their supervisory role, and so the brokerage may be liable for the full amount of the buyer’s earnest money.

- Let’s face it! Someone on the buyer’s side screwed up here, and now they are trying to cover their butts and avoid liability.

- Typically behind the scenes what would be happening is the buyer’s are getting obnoxious with their broker, telling their broker they want their earnest money back, and I can just hear them saying to their broker, “You promised we could get our earnest money back. What’s the delay?” And what is their broker saying? Probably something like, “We’re working on it. We dealing with the listing broker, and we’ve been working with our brokerage attorney. We’ll get back to you as soon as we have news.”

Let’s admit this: No broker/owner in his right mind would wait until after the closing date to issue a notice of the failure of financing. Not in a million years.

How Are These Cases Resolved?

If the parties don’t agree how the earnest money is to be released, the escrow company is required by law to tender the EM to the superior court, and then the buyer and seller have to hire their own attorneys to litigate the release of the money. Because the cost of attorney’s fees could exceed the EM, the parties usually negotiate a split of the EM that seems fair.

But when a buyer screws up as bad as the buyer and his broker did in this case, the seller might stick to their guns in order to get 100% of the EM, and to ask the court for a recovery of their attorney’s fees under the attorney’s fee provision in the contract.

The buyer risks not getting any of their EM, plus paying for their own attorney’s fees (easily $40,000 plus), and having to pay the attorney’s fees of the seller. All of this means it is sometimes wise to divide the EM in such a case 25% to the buyer and 75% to the seller, and be done with the whole dispute. Of course, if the buyer’s broker did screw up, the buyers could sue her and the brokerage. The brokerage’s errors and omissions insurance company would just write a check to the buyer to settle the case. That’s how it works. The E&O is always the deep pocket.

How many times have I written or said that buyers and sellers better be darn sure they hire a competent, honest, loyal, and professional broker who also knows contract law and how to keep their clients out of trouble?

Last Updated on August 12, 2022 by Chuck Marunde

{kind=link}

I’m buying for the first time in Washington and this line gave me such pause that I had to look for supplementary professional opinion. Thank you for your succinct and accessible writing – now my realtor won’t have to suffer my curiosity AND I have a better overall understanding of the implicit and explicit terms of my contract. 🙂

My pleasure SV. Glad you found this article helpful. Good luck my friend with your transaction.