Search Videos on The Real Estate Market and Where Prices Are Going

What is the state of the real estate market? Are prices headed up or down? Are listings staying on the...

What is the state of the real estate market? Are prices headed up or down? Are listings staying on the...

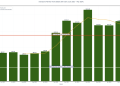

What is the Sequim Real Estate Market doing? How does it look with all our annual data for 2022 finally...

Will there be a housing recession? Are we in the beginning of a housing recession, and if so, how long...

Are buyers competing to bid prices up above current list prices? The answer is yes, at least for the nice...

Are we at the top of the real estate market right now? Are we in the midst of a real...

"Should I submit a backup offer?" is a question I hear in this seller's market, and it's a little different...

The Sequim real estate market has seen it's toughest year yet with high demand for the best homes in the...

I think you'll enjoy this short video with a Sequim Real Estate market update through the month of May 2020....

What will the Sequim real estate market bring us in 2019? I'm sure most real estate agents are afraid to...

The Sequim real estate market may be turning from a seller's market to a more balanced market, if not a...

If the stock market collapse is imminent, or at least on the near horizon, now is the time to take...

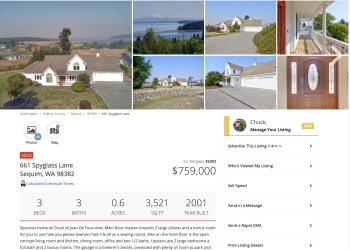

The Sequim real estate market is unique, and if you're thinking about buying a home in the Sequim area, it...

"Days on market" (or DOM) is a number that tells you how long a home has been listed on the market....

The Sequim real estate market in November is interesting. The number of active listings was down 22% from one year...

The Sequim real estate market report for August is especially revealing, because it shows the reality and consistency of the...

The Sequim real estate market continues its steady growth. During February the number of active listings was up 2% from...

The Sequim real estate market for December 2014 is interesting. Most Decembers tend to slow down, because closings in December...

This real estate market report covers September of 2014 and compares listings, volume, and prices to the prior month and...

Is the real estate market overvalued right now? According to the Chief Economist for Trulia, Jed Kolko, the real estate...

Sequim is in a bifurcated real estate market, and we are seeing a similar pattern in other parts of the...

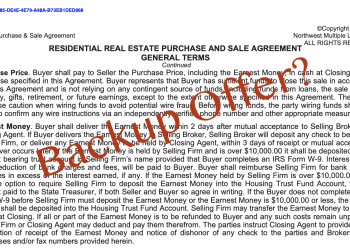

"I wish I read this before selling my

home. I could have saved $50,000." Andy

The largest independent real estate blog in the State of Washington with over 2,200 articles totally focused on our client’s best interest, their needs and their curiosity. All free and 100% reliable. I’m here if you need me,