Buying a Foreclosure and How Banks Kill Deals

Buying a foreclosure can be a very frustrating experience. Today I tell a true story about how a bank killed...

Buying a foreclosure can be a very frustrating experience. Today I tell a true story about how a bank killed...

Foreclosure ripoffs are out there, so be careful. They come in two forms. The first are the foreclosure ripoffs that...

HUD closing requirements are a nightmare scenario for buyers. If you think buying real estate from a normal human being...

Lawsuits against auction.com are coming, and there will be class action lawsuits and individual lawsuits, and it is going to...

Have you spotted a Fannie Mae foreclosure in the MLS that looks like it could be "the one"? Buying a...

What about Sequim foreclosures? Are there some opportunities for buyers with Sequim foreclosures? Today Zillow reported that 18.8% (almost one...

Is it hard to find a foreclosure that is a good deal in Sequim or Port Angeles? The short answer...

New rules are coming for the deed in lieu of foreclosure on March 1, 2013. If a loan modification or...

It makes sense to look at Sequim foreclosures and Port Angeles foreclosures if you are retiring and looking for the...

Looking at a Sequim foreclosure? Thinking about making an offer on a Sequim foreclosure? Think again, unless you have months...

Foreclosure help is available, although in the Sequim area we have very few foreclosures compared to everywhere else around the...

HUD homes are foreclosures that are now owned by HUD (Housing and Urban Development) and listed for sale by HUD. ...

Sequim investors cannot find great deals on homes in Sequim. They are literally unable to find good investment properties to...

The Sequim real estate market is a tough real estate market, but I have been observing a consistent pattern for...

Clallam County Foreclosures are small in number, among the lowest foreclosure rates in the United States. RealtyTrac just came out...

Sequim foreclosures make up a very small part of the market. We all hear about the massive number of foreclosures...

How to Buy a Foreclosure is a subject I've written about many times on this real estate blog, but today...

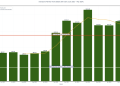

Foreclosure sales in Sequim and Port Angeles for the calendar year tell an interesting story, especially if you are retiring...

How can you find Sequim foreclosures? The Clallam County foreclosure market, including Sequim and Port Angeles is chaotic at best,...

People ask me if there are some great deals in Sequim foreclosures or Port Angeles foreclosures. The real estate market...

"I wish I read this before selling my

home. I could have saved $50,000." Andy

The largest independent real estate blog in the State of Washington with over 2,200 articles totally focused on our client’s best interest, their needs and their curiosity. All free and 100% reliable. I’m here if you need me,