Appraisal Management Companies

Appraisal management companies are the bane of a buyer's existence. This is the biggest problem right now for a buyer who...

Appraisal management companies are the bane of a buyer's existence. This is the biggest problem right now for a buyer who...

Today we have an article about reverse mortgages written by mortgage expert Buck Gieseke. Reverse mortgages are one of the...

The loan process is enough to turn a normal person into a zombie. You may have retired from a stressful...

The appeal of a VA loan is primarily the low down payment. Most conventional loans today will require a 20%...

Buyers often ask if owner financing is possible? Will sellers carry the paper? In other words, will sellers offer buyers owner...

Reverse mortgages are advertised every day on many cable and satellite channels, and the companies promoting reverse mortgages are using...

Mortgage problems are the rule, not the exception today. Even with perfect credit and a huge down payment, a mortgage broker is...

Today I'll explain how FNMA (Fannie Mae) is killing transactions by requiring private road maintenance agreements. Sequim, Washington is rural...

You might want to calculate the balance of a mortgage if you are thinking about buying a home that is...

I've written elsewhere about real estate bankruptcy and how to buy a home out of a bankruptcy. The purpose of...

How will the government shutdown effect real estate? Since many buyers will apply for a government insured (FHA) or guaranteed...

Cash has been King for a while, but the value of purchasing your home with cash has risen to entirely...

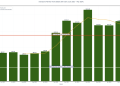

Mortgage rates are headed upward. There's no doubt about that. I'm no seer or son of a seventh son, but...

Mortgage rates have hit historical all-time lows during this recession, but mortgage rates appear to be headed upward. In late...

Most buyers select a local mortgage broker, but once in a great while I have a buyer who has a...

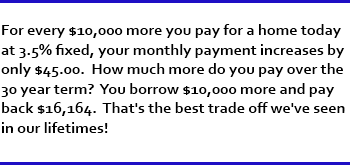

How much your monthly mortgage payment will be is often one of the primary factors in deciding how much of...

Seller financing has made a small comeback, and a few sellers are deciding to carry the loan for a buyer. ...

Most buyers will need a loan officer, but very few buyers realize how critical it is to chose the right...

Now that so many retirees of this generation are paying off their mortgages, the question often comes up, what happens...

Reverse Mortgages can be great for some retirees, and I've written about some of the dangers of reverse mortgages in...

"I wish I read this before selling my

home. I could have saved $50,000." Andy

The largest independent real estate blog in the State of Washington with over 2,200 articles totally focused on our client’s best interest, their needs and their curiosity. All free and 100% reliable. I’m here if you need me,